DATA 644 (Bayesian Reasoning in Data Science): Assignment 1

Contents

DATA 644 (Bayesian Reasoning in Data Science): Assignment 1#

%pip install pymc pytensor

Requirement already satisfied: pymc in /usr/local/lib/python3.10/dist-packages (5.7.2)

Requirement already satisfied: pytensor in /usr/local/lib/python3.10/dist-packages (2.14.2)

Requirement already satisfied: arviz>=0.13.0 in /usr/local/lib/python3.10/dist-packages (from pymc) (0.15.1)

Requirement already satisfied: cachetools>=4.2.1 in /usr/local/lib/python3.10/dist-packages (from pymc) (5.3.2)

Requirement already satisfied: cloudpickle in /usr/local/lib/python3.10/dist-packages (from pymc) (2.2.1)

Requirement already satisfied: fastprogress>=0.2.0 in /usr/local/lib/python3.10/dist-packages (from pymc) (1.0.3)

Requirement already satisfied: numpy>=1.15.0 in /usr/local/lib/python3.10/dist-packages (from pymc) (1.25.2)

Requirement already satisfied: pandas>=0.24.0 in /usr/local/lib/python3.10/dist-packages (from pymc) (1.5.3)

Requirement already satisfied: scipy>=1.4.1 in /usr/local/lib/python3.10/dist-packages (from pymc) (1.11.4)

Requirement already satisfied: typing-extensions>=3.7.4 in /usr/local/lib/python3.10/dist-packages (from pymc) (4.9.0)

Requirement already satisfied: setuptools>=48.0.0 in /usr/local/lib/python3.10/dist-packages (from pytensor) (67.7.2)

Requirement already satisfied: filelock in /usr/local/lib/python3.10/dist-packages (from pytensor) (3.13.1)

Requirement already satisfied: etuples in /usr/local/lib/python3.10/dist-packages (from pytensor) (0.3.9)

Requirement already satisfied: logical-unification in /usr/local/lib/python3.10/dist-packages (from pytensor) (0.4.6)

Requirement already satisfied: miniKanren in /usr/local/lib/python3.10/dist-packages (from pytensor) (1.0.3)

Requirement already satisfied: cons in /usr/local/lib/python3.10/dist-packages (from pytensor) (0.4.6)

Requirement already satisfied: matplotlib>=3.2 in /usr/local/lib/python3.10/dist-packages (from arviz>=0.13.0->pymc) (3.7.1)

Requirement already satisfied: packaging in /usr/local/lib/python3.10/dist-packages (from arviz>=0.13.0->pymc) (23.2)

Requirement already satisfied: xarray>=0.21.0 in /usr/local/lib/python3.10/dist-packages (from arviz>=0.13.0->pymc) (2023.7.0)

Requirement already satisfied: h5netcdf>=1.0.2 in /usr/local/lib/python3.10/dist-packages (from arviz>=0.13.0->pymc) (1.3.0)

Requirement already satisfied: xarray-einstats>=0.3 in /usr/local/lib/python3.10/dist-packages (from arviz>=0.13.0->pymc) (0.7.0)

Requirement already satisfied: python-dateutil>=2.8.1 in /usr/local/lib/python3.10/dist-packages (from pandas>=0.24.0->pymc) (2.8.2)

Requirement already satisfied: pytz>=2020.1 in /usr/local/lib/python3.10/dist-packages (from pandas>=0.24.0->pymc) (2023.4)

Requirement already satisfied: toolz in /usr/local/lib/python3.10/dist-packages (from logical-unification->pytensor) (0.12.1)

Requirement already satisfied: multipledispatch in /usr/local/lib/python3.10/dist-packages (from logical-unification->pytensor) (1.0.0)

Requirement already satisfied: h5py in /usr/local/lib/python3.10/dist-packages (from h5netcdf>=1.0.2->arviz>=0.13.0->pymc) (3.9.0)

Requirement already satisfied: contourpy>=1.0.1 in /usr/local/lib/python3.10/dist-packages (from matplotlib>=3.2->arviz>=0.13.0->pymc) (1.2.0)

Requirement already satisfied: cycler>=0.10 in /usr/local/lib/python3.10/dist-packages (from matplotlib>=3.2->arviz>=0.13.0->pymc) (0.12.1)

Requirement already satisfied: fonttools>=4.22.0 in /usr/local/lib/python3.10/dist-packages (from matplotlib>=3.2->arviz>=0.13.0->pymc) (4.48.1)

Requirement already satisfied: kiwisolver>=1.0.1 in /usr/local/lib/python3.10/dist-packages (from matplotlib>=3.2->arviz>=0.13.0->pymc) (1.4.5)

Requirement already satisfied: pillow>=6.2.0 in /usr/local/lib/python3.10/dist-packages (from matplotlib>=3.2->arviz>=0.13.0->pymc) (9.4.0)

Requirement already satisfied: pyparsing>=2.3.1 in /usr/local/lib/python3.10/dist-packages (from matplotlib>=3.2->arviz>=0.13.0->pymc) (3.1.1)

Requirement already satisfied: six>=1.5 in /usr/local/lib/python3.10/dist-packages (from python-dateutil>=2.8.1->pandas>=0.24.0->pymc) (1.16.0)

%matplotlib inline

import warnings

import arviz as az

import matplotlib as mpl

import matplotlib.pyplot as plt

import numpy as np

import pymc as pm

#import theano.tensor as tt

from pymc import Model, Normal, Slice, sample, HalfNormal

from pymc.distributions import Interpolated

from scipy import stats

#from theano import as_op

import pickle

from google.colab import files

import pickle

uploaded = files.upload()

Saving my_arrays.pkl to my_arrays.pkl

with open("my_arrays.pkl", 'rb') as file:

data = pickle.load(file)

import numpy as np

np.shape(data['X1'])

(1000,)

X1 = data['X1']

X2 = data['X2']

Y = data['Y']

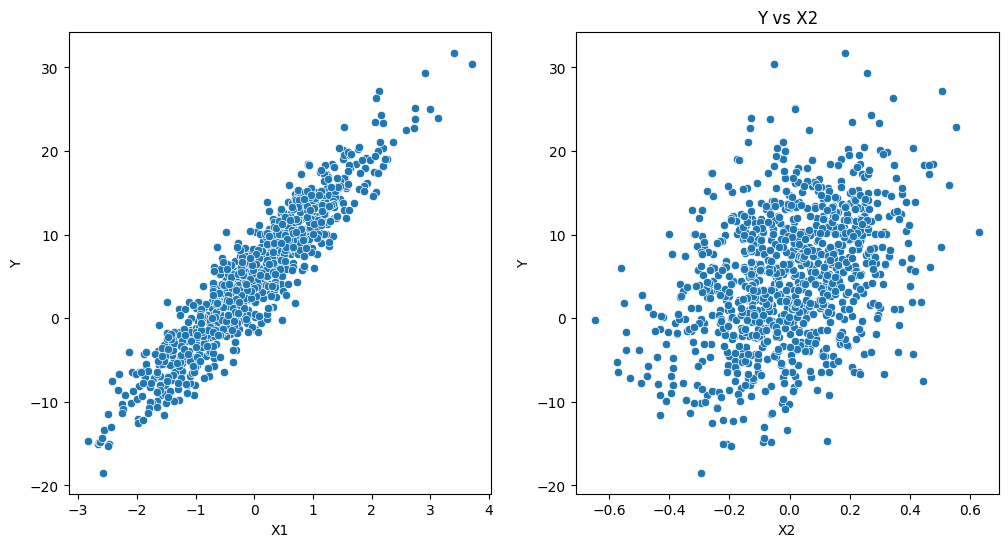

Visual inspection#

import pandas as pd

import statsmodels.api as sm

import seaborn as sns

# Create a DataFrame from the arrays

data = pd.DataFrame({

'X1': X1,

'X2': X2,

'Y': Y

})

# Prepare the features and target variable

X = data[['X1', 'X2']]

X = sm.add_constant(X) # Adds a constant term to the predictor

Y = data['Y']

# Visualization

plt.figure(figsize=(12, 6))

# Plot Y vs X1

plt.subplot(1, 2, 1)

sns.scatterplot(x='X1', y='Y', data=data)

# Plot Y vs X2

plt.subplot(1, 2, 2)

sns.scatterplot(x='X2', y='Y', data=data)

plt.title('Y vs X2')

plt.show()

#---- you can also do a linear fit, etc. (complete)

# Perform linear regression

model = sm.OLS(Y, X).fit()

# Print the summary to inspect the coefficients and model performance

print(model.summary())

OLS Regression Results

==============================================================================

Dep. Variable: Y R-squared: 0.984

Model: OLS Adj. R-squared: 0.984

Method: Least Squares F-statistic: 3.081e+04

Date: Tue, 20 Feb 2024 Prob (F-statistic): 0.00

Time: 15:21:11 Log-Likelihood: -1395.6

No. Observations: 1000 AIC: 2797.

Df Residuals: 997 BIC: 2812.

Df Model: 2

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 5.0115 0.031 161.944 0.000 4.951 5.072

X1 7.0540 0.031 229.558 0.000 6.994 7.114

X2 12.8148 0.155 82.457 0.000 12.510 13.120

==============================================================================

Omnibus: 0.260 Durbin-Watson: 2.042

Prob(Omnibus): 0.878 Jarque-Bera (JB): 0.335

Skew: -0.027 Prob(JB): 0.846

Kurtosis: 2.929 Cond. No. 5.10

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Building the Model#

basic_model = Model()

with basic_model:

# Priors for unknown model parameters

alpha = Normal("alpha", mu=0, sigma=10)

beta0 = Normal("beta0", mu=0, sigma=10)

beta1 = Normal("beta1", mu=0, sigma=10)

sigma = HalfNormal("sigma",sigma=5)

# Expected value of outcome

mu = alpha + beta0 * X1 + beta1 * X2

# Likelihood (sampling distribution) of observations

Y_obs = Normal("Y_obs", mu=mu, sigma=sigma, observed=Y)

# draw 1000 posterior samples

trace_in = sample(5000)

100.00% [6000/6000 00:07<00:00 Sampling chain 0, 0 divergences]

100.00% [6000/6000 00:06<00:00 Sampling chain 1, 0 divergences]

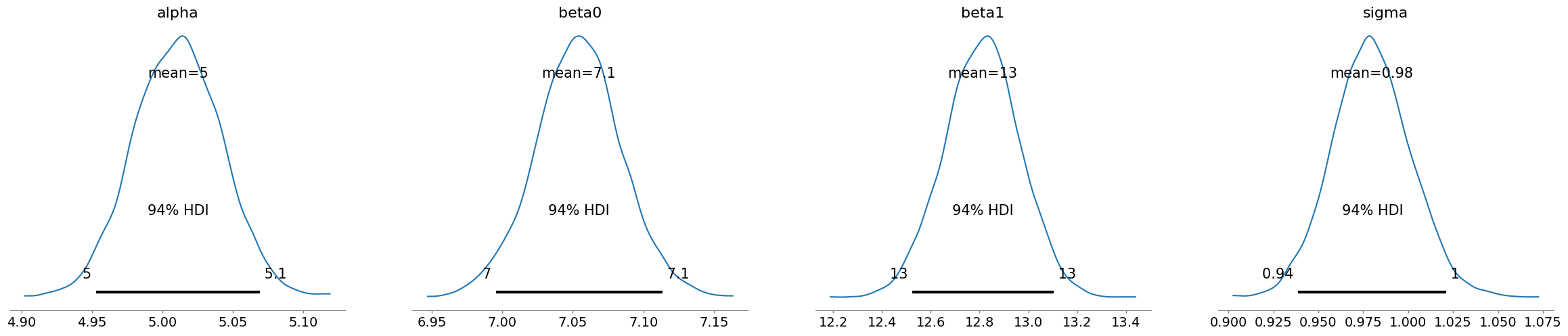

az.plot_posterior(trace_in)

/usr/local/lib/python3.10/dist-packages/arviz/utils.py:184: NumbaDeprecationWarning: The 'nopython' keyword argument was not supplied to the 'numba.jit' decorator. The implicit default value for this argument is currently False, but it will be changed to True in Numba 0.59.0. See https://numba.readthedocs.io/en/stable/reference/deprecation.html#deprecation-of-object-mode-fall-back-behaviour-when-using-jit for details.

numba_fn = numba.jit(**self.kwargs)(self.function)

array([<Axes: title={'center': 'alpha'}>,

<Axes: title={'center': 'beta0'}>,

<Axes: title={'center': 'beta1'}>,

<Axes: title={'center': 'sigma'}>], dtype=object)

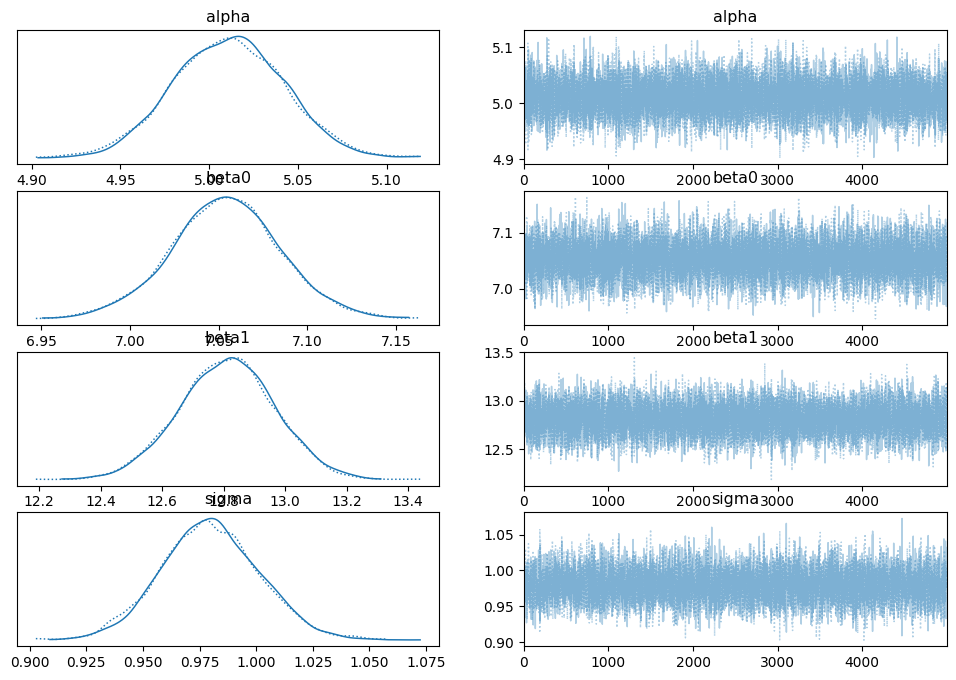

az.plot_trace(trace_in, compact=True)

array([[<Axes: title={'center': 'alpha'}>,

<Axes: title={'center': 'alpha'}>],

[<Axes: title={'center': 'beta0'}>,

<Axes: title={'center': 'beta0'}>],

[<Axes: title={'center': 'beta1'}>,

<Axes: title={'center': 'beta1'}>],

[<Axes: title={'center': 'sigma'}>,

<Axes: title={'center': 'sigma'}>]], dtype=object)

np.shape(X1)

(1000,)

plt.hist(X1)

(array([ 18., 55., 122., 230., 248., 194., 95., 29., 6., 3.]),

array([-2.83591463, -2.18122708, -1.52653953, -0.87185197, -0.21716442,

0.43752313, 1.09221068, 1.74689823, 2.40158578, 3.05627333,

3.71096089]),

<BarContainer object of 10 artists>)

az.summary(trace_in,hdi_prob=0.94)

| mean | sd | hdi_3% | hdi_97% | mcse_mean | mcse_sd | ess_bulk | ess_tail | r_hat | |

|---|---|---|---|---|---|---|---|---|---|

| alpha | 5.011 | 0.031 | 4.953 | 5.069 | 0.000 | 0.000 | 17161.0 | 7772.0 | 1.0 |

| beta0 | 7.054 | 0.031 | 6.995 | 7.114 | 0.000 | 0.000 | 15873.0 | 8126.0 | 1.0 |

| beta1 | 12.811 | 0.154 | 12.525 | 13.103 | 0.001 | 0.001 | 14779.0 | 8785.0 | 1.0 |

| sigma | 0.980 | 0.022 | 0.939 | 1.021 | 0.000 | 0.000 | 11961.0 | 8264.0 | 1.0 |

What happens if using 10 observations only?#

# Generate 10 random unique indices from the range of your data length

random_indices = np.random.choice(len(X1), 10, replace=False)

# Select the corresponding elements from X1, X2, and Y

selected_X1 = X1[random_indices]

selected_X2 = X2[random_indices]

selected_Y = Y.values[random_indices]

selected_model = Model()

with selected_model:

# Priors for unknown model parameters

alpha = Normal("alpha", mu=0, sigma=10)

beta0 = Normal("beta0", mu=0, sigma=10)

beta1 = Normal("beta1", mu=0, sigma=10)

sigma = HalfNormal("sigma",sigma=5)

# Expected value of outcome

mu = alpha + beta0 * selected_X1 + beta1 * selected_X2

# Likelihood (sampling distribution) of observations

Y_obs = Normal("Y_obs", mu=mu, sigma=sigma, observed=selected_Y)

# draw 1000 posterior samples

trace_selected = sample(5000)

100.00% [6000/6000 00:08<00:00 Sampling chain 0, 1 divergences]

100.00% [6000/6000 00:09<00:00 Sampling chain 1, 0 divergences]

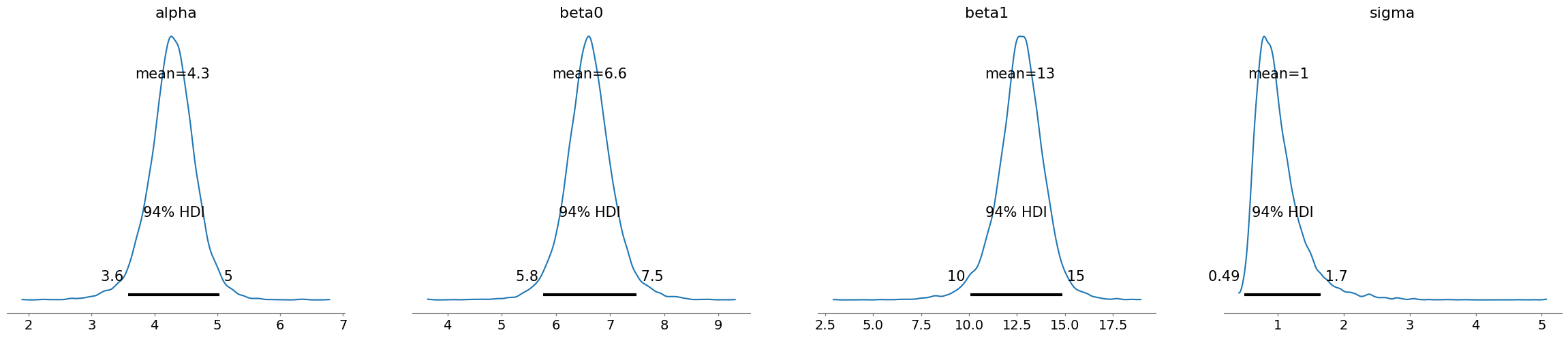

az.plot_posterior(trace_selected)

array([<Axes: title={'center': 'alpha'}>,

<Axes: title={'center': 'beta0'}>,

<Axes: title={'center': 'beta1'}>,

<Axes: title={'center': 'sigma'}>], dtype=object)

az.summary(trace_selected,hdi_prob=0.94)

| mean | sd | hdi_3% | hdi_97% | mcse_mean | mcse_sd | ess_bulk | ess_tail | r_hat | |

|---|---|---|---|---|---|---|---|---|---|

| alpha | 4.283 | 0.385 | 3.581 | 5.033 | 0.005 | 0.004 | 6071.0 | 4790.0 | 1.0 |

| beta0 | 6.620 | 0.453 | 5.761 | 7.487 | 0.006 | 0.004 | 6391.0 | 4463.0 | 1.0 |

| beta1 | 12.654 | 1.270 | 10.052 | 14.876 | 0.017 | 0.012 | 5998.0 | 4707.0 | 1.0 |

| sigma | 1.006 | 0.370 | 0.493 | 1.653 | 0.006 | 0.004 | 3700.0 | 4565.0 | 1.0 |

The HDI intervals become broader, highlighting more uncertainty (less observations means less information we could leverage on in our model)